- Professional Blogs

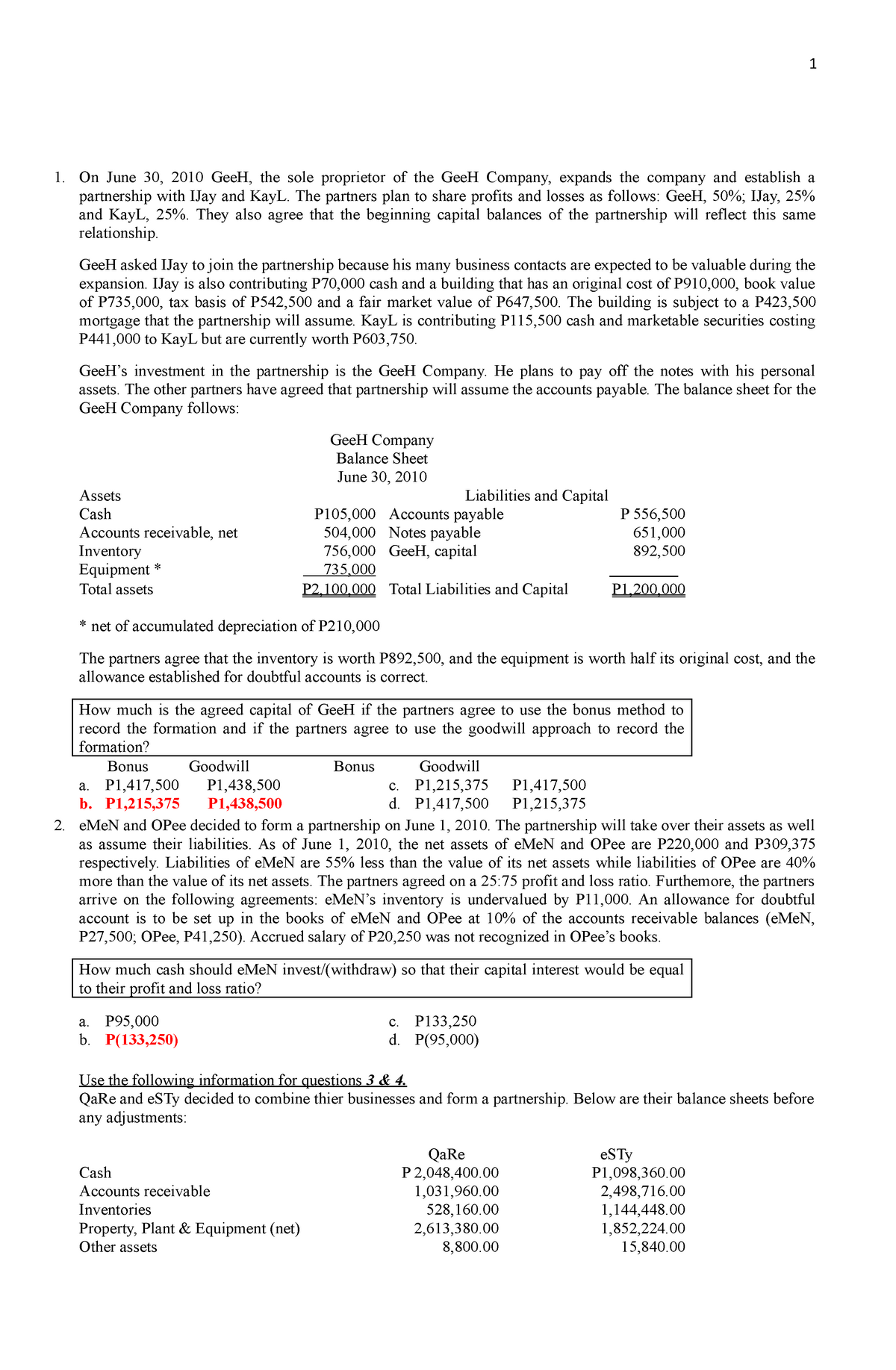

- First-time Consumers

If you are British mortgage company might have come loosening its lending conditions following the cutbacks when you look at the 2020, that of amount is that providing home financing simply isn’t as as simple it once was.

To make homeownership less costly, one to option you may also thought is actually a simultaneous applicant financial. Whether or not trickier to come by, with the aid of a brokerage it’s yes something to explore when you find yourself hoping to get a feet on the hierarchy.

This article teaches you the pros and you will drawbacks off multiple-candidate mortgage loans, how-to begin wanting you to, and just what options you can also thought.

What’s a multiple-applicant home loan?

A multiple-applicant or multiple-person’ financial are home financing which is mutual ranging from over two people. Everyone could be named towards property deeds and everyone is jointly responsible for the borrowed funds payments.

Who will score a multiple applicant home loan?

You can now sign up for a multiple-applicant home loan – although it’s best to consult with an agent you see hence loan providers promote these things.

Just like any home loan, every parties inside it will need to fulfill lender standards, and there’s a risk of getting rejected for those who otherwise that or higher of your co-candidates features less than perfect credit, cost things otherwise have a tendency to go beyond the utmost many years maximum during the home loan identity.

There are no limitations towards the who you get a multi-candidate mortgage which have, whether it is a partner, loved ones, nearest and dearest, otherwise organization couples.

Having said that, it’s important to think hard ahead of getting into an agreement once the there can be extreme effects in your economic coming.

Just how many individuals should be named towards the home financing?

cuatro is usually the restrict level of people, but criteria are different by bank. Some might only feel willing to undertake over two applicants when they blood household members, otherwise there is certainly most other stipulations affixed.

When you are trying to get a parallel-candidate mortgage to your intention out-of improving your value, be aware that even though some loan providers are happy to possess multiple individuals to getting https://paydayloanalabama.com/mosses/ titled for the label deeds, they may limitation the amount of candidates whoever income represents getting value intentions.

How can multi-candidate mortgages differ from standard mortgages?

Generally speaking, multi-individual financial prices and costs are like regarding good standard financial. However, that have more than one people with the deeds gives you to mix your deals and put down a bigger deposit, that definitely change the pricing you may be offered.

The greater the put, the greater aggressive new prices shall be. Like, for people who save yourself an excellent 15% put and one applicant conserves ten%, you will need a beneficial 75% LTV (Loan so you’re able to Really worth) home loan. This needs to be comparatively cheaper than brand new 85% LTV mortgage might was basically capable afford once the an individual applicant.

This new coupons is going to be such significant to have first-day customers, in which having fun with shared coupons to go of good 95% to help you a beneficial 90% LTV mortgage otherwise lower will make a big difference and you will conserve you a lot of money.

How much do you really use for a multiple-candidate financial?

Whenever choosing just how much you can borrow on a multiple-person financial, many loan providers will only consider the a couple of higher money earners and you will apply financing cover based on a simultaneous of their mutual wages.

That said, you’ll find loan providers available who can take all applicants’ income into consideration, however it is better to run a brokerage to identify the best option bank, since the enhanced chance posed from the additional income could mean high costs.