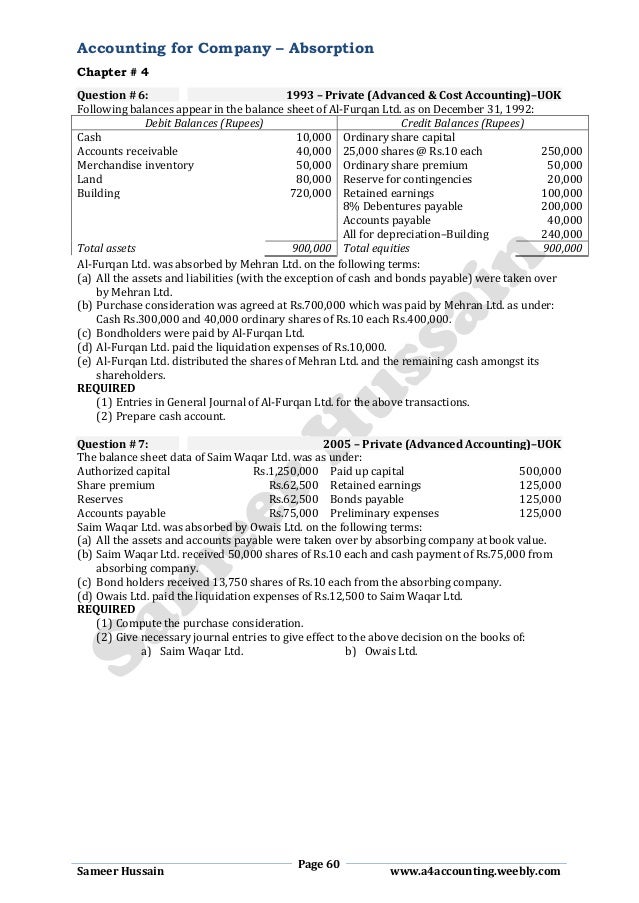

W hen considering attempting to sell your property in the Alberta, that have an enthusiastic assumable mortgage are going to be a unique feature in order to notice potential buyers. Selling property which have an assumable home loan allows the customer in order to take over the fresh new seller’s mortgage beneath the same words, which can be such as for example enticing within the an industry in which rates was higher or increasing. Why don’t we speak about how an assumable home loan functions, just what pros and cons to help you be the cause of, and how manufacturers is also control this feature in order to probably facilitate its house marketing.

Having informational purposes simply. Constantly consult with a licensed home loan or mortgage top-notch before proceeding with any a property transaction.

What $255 payday loans online same day New Hampshire is an Assumable Mortgage?

While a preexisting financial lets a beneficial homebuyer when planning on taking across the most recent customer’s financial terms. Basically, the borrowed funds (and its own rate of interest) is being offered as well as the property. It’s an extremely official kind of money that isn’t extremely aren’t used in Canada, nevertheless can do just fine regarding correct products.

According to the newest owner’s equity home, the fresh new down payment from the customer can differ. The buyer accounts for make payment on difference between the latest an excellent home loan and the residence’s worth.

Like, in case the cost is actually $800,000 plus the family has actually a left home loan harmony from $500,000, the buyer need to pay $three hundred,000 into the provider initial (or work out a fees plan with the supplier). It is a much larger amount than the usual 20% advance payment out of $160,000 toward an $800,000 family, and may need the visitors to take out the second home loan. On the other hand, in case the merchant have very little security home, eg whenever selling a house following to invest in, the buyer can pick a home that have much down out-of-wallet costs.

Of the and if the borrowed funds, the buyer can be miss out the challenge and you may charges out of obtaining another type of mortgage and you can instead action to the boots of prior proprietor about your financing. This might be such as for instance useful in the event the established interest is gloomier compared to the latest financial rates, possibly preserving individuals money in the near future.

Vendors, on the other hand, will dsicover assumable mortgage loans useful as it can be utilized while the a feature if your interest levels are extremely advantageous, focus a unique pond away from potential customers, and avoid prepayment punishment to the home loan.

And this Mortgages Was Assumable?

In short, an enthusiastic assumable home loan are one financial that financial allows an alternative debtor when deciding to take more. In the event the a mortgage lender actually ready to allow financial feel assumed, they will have a condition regarding the mortgage package stating therefore. Basically, presumption conditions for the home loan deals identify both the financial do not getting thought without the the newest customer being qualified with the mortgage, otherwise that the home loan have to be given out through to the new income of the house (and thus can’t be thought).

Generally speaking, subject to bank approval, most fixed-rate mortgages within the Canada is thought, while varying-price mortgages and you may home security funds dont.

If you find yourself looking for selling your house with an assumable financial, start with asking about the option along with your bank.

Masters & Drawbacks of Selling That have a keen Assumable Mortgage loans

In relation to promoting which have an assumable home loan in the Canada, you should weigh the pros and you may cons very carefully when you look at the framework of your own newest real estate market along with your financial predicament.

Advantages

Vendors benefit from drawing an alternate pond regarding audience which have assumable mortgages because of the attractiveness of lower-rates fund. By offering an assumable home loan, providers can make their property more appealing in order to people looking to benefit from beneficial interest rates. This can lead to a quicker marketing and potentially a higher price point. As well, providers is end mortgage prepayment penalties by permitting people to imagine its mortgage.

Consumers, additionally, may benefit regarding of course a mortgage whenever current rates is actually more than the original loan’s rate, going for high savings along side longevity of the borrowed funds. They could along with prevent investing charge linked to undertaking yet another mortgage.

Disadvantages

You to definitely biggest prospective downside to own going for an assumable mortgage when selling a property inside Canada is the fact suppliers can be produced liable whether your the fresh new borrower non-payments for the thought mortgage. Mortgage loans try property lien; if for example the client try economically irresponsible and also the family doesn’t afterwards sell for sufficient to safeguards the mortgage, the lender is legitimately need you to spend the money for difference because the the original debtor. When you’re worried about this opportunity, go after a launch demand from your own financial that release your from potential responsibility.

Consumers wanting if in case the current financing you are going to run into pressures for example as searching for a hefty down payment otherwise an extra financial.

While you are providers might stop prepayment penalties by permitting assumption, they may remain vulnerable to monetary effects in the event your the latest debtor injuries the house or property or does not build money. Consider these points carefully before carefully deciding to your an assumable home loan having selling your home.

Promoting your house in the Canada with a keen assumable home loan is going to be good option for both manufacturers and you can buyers throughout the right products, spending less and streamlining the closure processes.

Although not, it is essential to carefully think about the terms of the fresh new assumable mortgage and make certain all of the functions are-advised. Seeking suggestions out of realtors can help improve purchase much easier and productive.

To have informative purposes simply. Usually consult an authorized mortgage otherwise financial professional before proceeding with people a house purchase.